BC is home to some of the most breathtaking landscapes and world-famous bike parks and trails. It goes without saying that we love the outdoors here and many of us take advantage of the abundance of options for avid mountain bikers, road cyclists and casual city riders alike. A bike is an important asset for many of us, and like other valuable personal property, it’s worth taking measures to protect its value in the event of damage or theft.

When, if ever, have you thought about insurance for your bicycle? Many cyclists are unaware of the coverage they may need or the insurance they might already have. Here is what you should know:

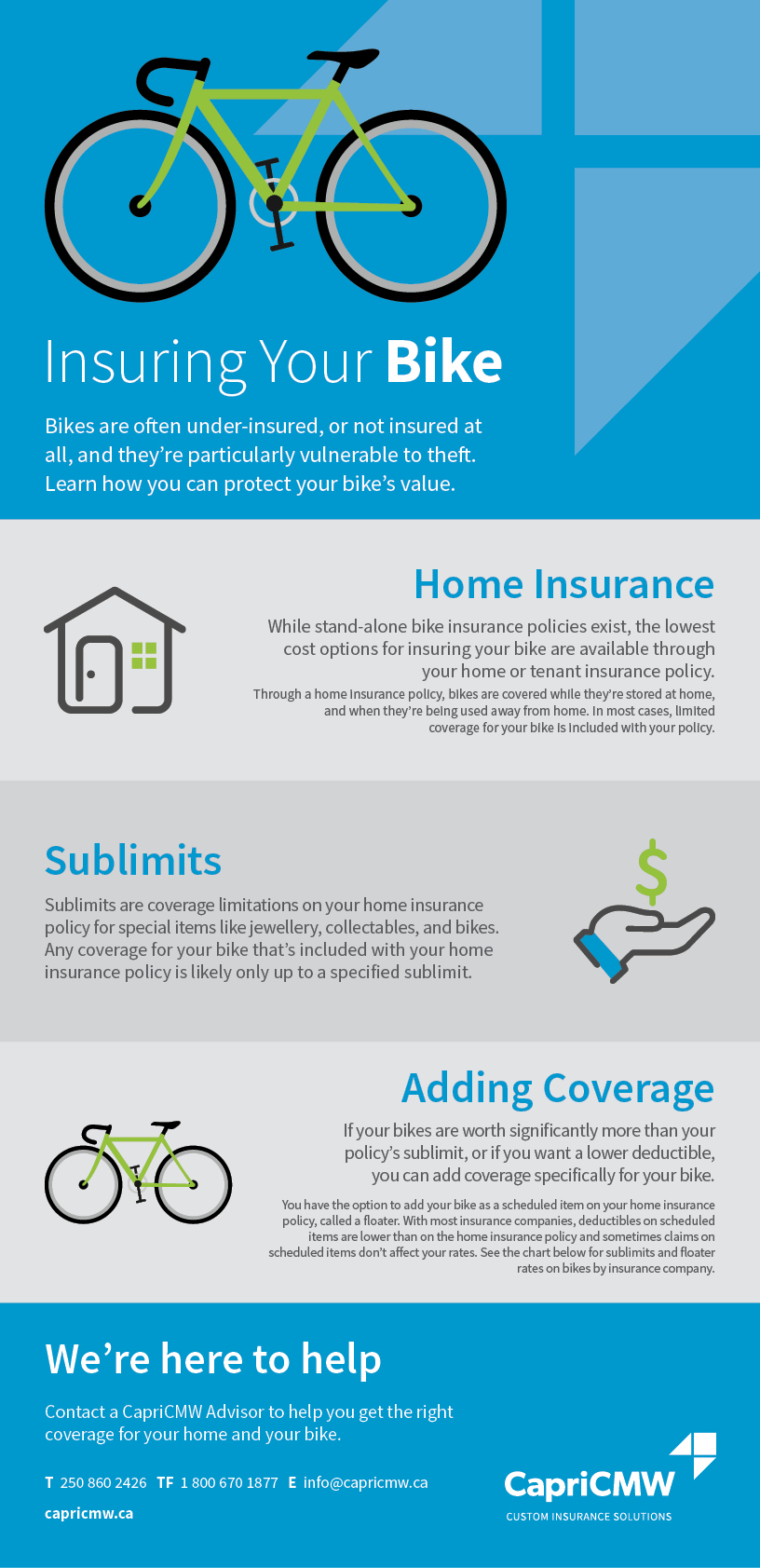

- Under comprehensive homeowner’s and tenant’s insurance, there is usually coverage for bikes up to a certain amount, known as a sub-limit, for theft, mysterious disappearance and damage from attempted theft.

- Your bike is covered both while being stored at home and when it’s being used outside of the home. That means if your bike is stolen from your vehicle, or from a public area, you have coverage.

- If you require additional coverage for your bike above the sub-limits included in your homeowner’s or tenant’s insurance, you can add your bike as a scheduled item, called a ‘floater’. Floater rates vary between insurance companies, and often come with lower deductibles than the homeowner’s policy deductible. Depending on the insurance provider, making a claim for your bicycle will not affect your premium.

- Bicycles are typically covered under homeowner’s or tenant’s insurance policies. There are very limited options available for standalone policies.

Our infographic below illustrates the options offered by some of the largest insurance providers offering bike coverage. You can also learn more about protecting your bike from theft and maximizing your chance of recovery by reading "Best Practices to Protect Your Bike from Thieves."

Our Advisors are here to help you find the right coverage for your bike. Contact CapriCMW to learn more about your options:

T: 1 800 670 1877

E: info@capricmw.ca